How to Negotiate Your First VC Term Sheet Without Losing Control of Your Startup

If a term sheet landed in your inbox today, would you sign it as is or pause and question it?

That decision, often made in a few days, can shape how your company operates for years. Not just in terms of ownership, but in how decisions are made, who gets a say, and what happens when things don’t go as planned.

Founders usually spend months preparing to raise capital, but very little time preparing to evaluate the terms that come with it. That gap is where control is given away.

A VC term sheet is not just about funding. It is about defining the relationship between the founder and the investor from day one.

What is a VC Term Sheet and How It Works

A startup funding term sheet is a document that outlines the key terms under which an investor agrees to invest in your company. It covers valuation, equity, governance rights, and investor protections.

While most parts of the document are non-binding at this stage, they set the structure for final legal agreements. Once signed, reversing unfavourable terms becomes difficult.

Understanding what is a VC term sheet helps founders approach it with the seriousness it deserves. It is not a formality. It is the foundation of your future cap table and control structure.

If you understand how a term sheet works, you start seeing it less as a document to accept and more as a framework to shape.

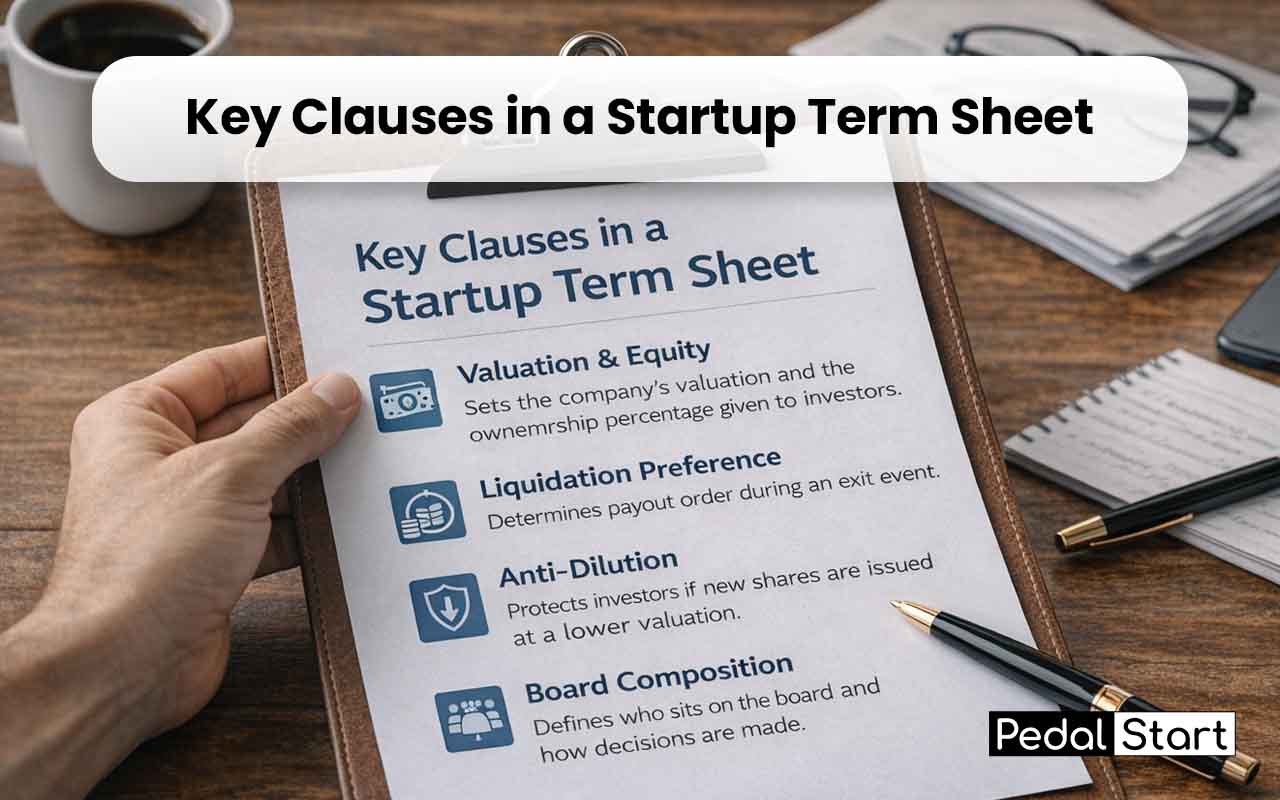

Key Clauses in a Startup Term Sheet

Every investor term sheet of a VC for startups includes a few core components that define how the deal works.

Valuation and equity determine how much ownership you are giving up. This is where most attention goes, but it is only one part of the equation.

Liquidation preference decides how proceeds are distributed during an exit. A standard structure protects investors without heavily impacting founders, but variations can change outcomes significantly.

Anti-dilution clauses protect investors if future rounds happen at lower valuations. The details here matter, especially in uncertain markets.

Board composition determines who influences major decisions. Even a single board seat can affect how control evolves over time.

These term sheet clauses startup founders agree to often have a longer impact than the valuation itself.

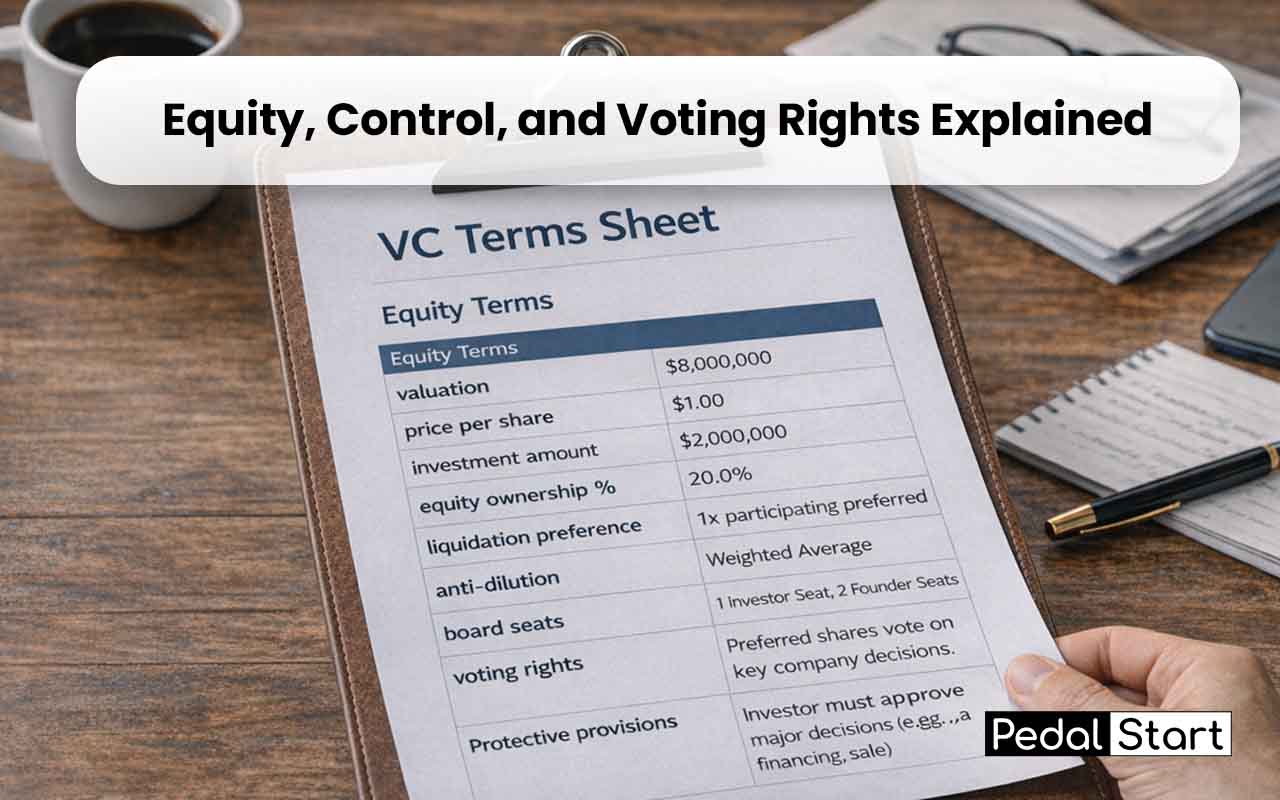

Equity, Control, and Voting Rights Explained

Ownership percentage is easy to measure. Control is not.

A founder can still hold a large share of the company and yet have limited authority if voting rights and board structures are not carefully considered.

Protective provisions are a common example. These clauses allow investors to approve or block specific decisions such as raising additional capital, entering new markets, or selling the company.

This is where reading an investor term sheet in detail becomes critical. The language around rights, approvals, and governance determines how flexible you remain as the company grows.

Looking at a sample VC term sheet helps build familiarity with how these rights are typically structured and where founders should pay closer attention.

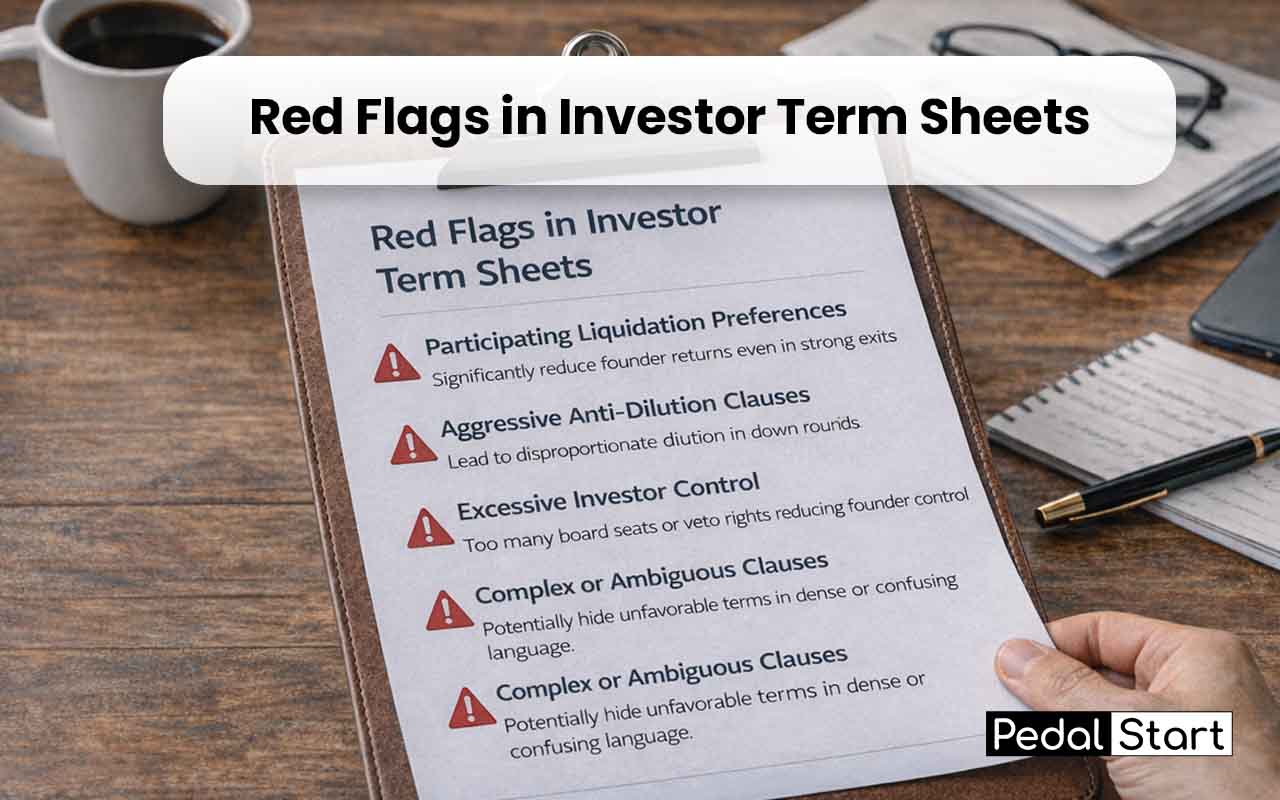

Red Flags in Investor Term Sheets

Some terms deserve immediate scrutiny.

Participating liquidation preferences can reduce founder returns significantly even in successful exits.

Aggressive anti-dilution clauses can lead to disproportionate dilution if the company raises at a lower valuation later.

Excessive investor control through board seats or veto rights can slow down decision-making and limit founder autonomy.

Another subtle red flag is complexity. If a clause is difficult to interpret, it is worth slowing down and seeking clarity before moving forward.

Recognizing these patterns early can prevent long-term complications.

How to Negotiate a VC Term Sheet

Knowing how to negotiate a VC term sheet is less about confrontation and more about clarity.

The first step is understanding what is standard at your stage. Early-stage deals often follow broad norms, and awareness helps anchor the conversation.

The second step is focusing on what truly matters. Founders do not need to negotiate every clause. The priority should be on terms that affect control, dilution, and future flexibility.

The third step is communication. Explaining why a certain structure works better for the business often leads to more productive discussions than simply pushing back.

Having experienced operators or mentors involved at this stage can also help identify terms that are easy to overlook but important in the long run.

Mistakes Founders Make During Negotiation

A common mistake is treating valuation as the only metric that matters. A higher valuation with restrictive terms can create more problems than a balanced deal.

Another mistake is moving too fast. Momentum feels important, but rushing through a term sheet often leads to missed details.

Some founders hesitate to ask questions, assuming it may slow down the process. In reality, clarity builds confidence on both sides.

Ignoring how terms play out in future rounds is another gap. What feels acceptable today may become restrictive later.

Understanding what founders should look for in a term sheet helps avoid these situations and approach negotiations with more confidence.

Conclusion

A VC term sheet is not just a milestone in fundraising. It is a decision point that defines how your company will be built.

Taking the time to understand, question, and shape it is not overthinking. It is part of building a company that you can continue to lead on your own terms.